Last updated: 3 March 2026

Most “fund formation” pain is not legal theory. It’s execution.

The structure looks fine on a diagram, but then:

– bank onboarding stalls,

– counterparties ask basic questions no one prepared for,

– approvals are unclear,

– records are scattered,

– and the fund becomes unmanageable as soon as it gets busy.

This is what we mean by a “bankable” structure: a fund or private investment vehicle that can be explained, evidenced, and operated cleanly year after year.

If you’re exploring a Hong Kong structure, start with our Investment Funds practice page:

—

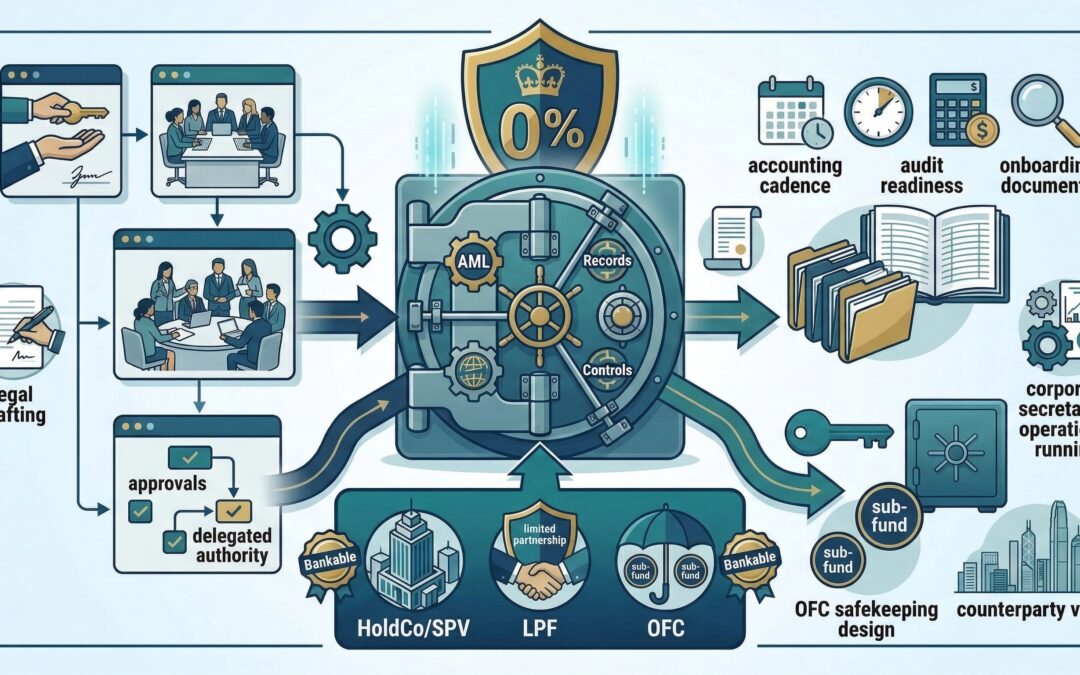

The 3 pillars of bankability

Pillar 1: A control story that makes sense (who can do what)

Banks and counterparties want to know:

– who has authority to instruct movements of money,

– who approves investments and disposals,

– what internal approvals exist (and whether they’re documented),

– how conflicts are handled.

This is governance, not “legal decoration”.

If you’re structuring a holding stack, our Corporate & Commercial practice often supports this layer:

Pillar 2: Records that exist before you need them

When onboarding or a review happens, you don’t get time to build records retroactively.

In practice you need:

– an approvals log (what was approved, when, by whom),

– an investor onboarding pack (CDD, declarations, source-of-wealth/source-of-funds support),

– clean accounting cadence (monthly/quarterly),

– audit readiness.

If regulatory mapping is relevant, our Regulatory practice can help:

Pillar 3: Asset and cash safekeeping mechanics (especially for OFCs)

If you’re using an OFC, custody and safekeeping design is central to whether the structure works.

Start with:

—

The “Bankable Structure Checklist” (forwardable to clients)

1) Governance Pack

– structure chart (entities + roles)

– signatory matrix (bank + internal approvals)

– delegated authority rules (what management can do without board approval)

– conflicts policy

– template minutes / written resolutions

2) AML & onboarding narrative pack

– source-of-wealth/source-of-funds narrative that matches the structure

– supporting documents organised and consistent

– investor classification approach (where relevant)

3) Operational cadence

– monthly bookkeeping rhythm

– quarterly governance review

– annual audit timeline

– compliance calendar (filings, renewals, registers)

—

Why this is where TITUS × IMSG becomes a better partner model

Many firms can draft documents.

Fewer firms help clients keep the structure clean and credible over time.

TITUS supports legal formation and operating documentation for funds:

Our sister team – IMSG supports the operating layer that keeps structures “alive”:

– company secretarial and filings,

– accounting/tax coordination,

– internal controls and reporting rhythm,

– practical readiness for banking and counterparties.

—

Which vehicle is easiest to keep bankable?

It depends on facts, but broadly:

– HoldCo + SPVs: simplest operationally if governance is designed properly.

– LPF: bankable when roles/records/authority are tight.

– OFC: bankable when custodian + investment manager sequencing is done early.

If you’re choosing, start here:

Hong Kong Funds & Private Investment Vehicles guide

—

Next step: quick call with our Principal

If you want to discuss a client fact pattern or your firm’s recurring needs, we can set up a quick Zoom call with Michael Titus (Principal, TITUS): https://titus.com.hk/our-people/michael-titus/

Send 2–3 time slots to us via:

Email: info@titus.com.hk, or

Whatsapp: +852 9702 3003

—

Disclaimer: This article is for general information only and does not constitute legal advice. Specific advice should be sought for your particular circumstances.

RELATED READING

– Pillar guide: Hong Kong Funds & Private Investment Vehicles guide

– LPF guide: LPF (Limited Partnership Fund) guide

– OFC guide: OFC (Open-Ended Fund Company) guide

– DIPN 61 (plain English): DIPN 61 explained (Unified Fund Exemption)