Last updated: 13 March 2026

“0% carried interest” is one of the most misunderstood headlines in Hong Kong funds marketing.

The reality is more nuanced:

– there is a carried interest concession regime,

– it has effective dates and conditions,

– and it’s designed to reward genuine asset management activity with real substance and governance.

If you’re considering a Hong Kong fund platform, start here:

—

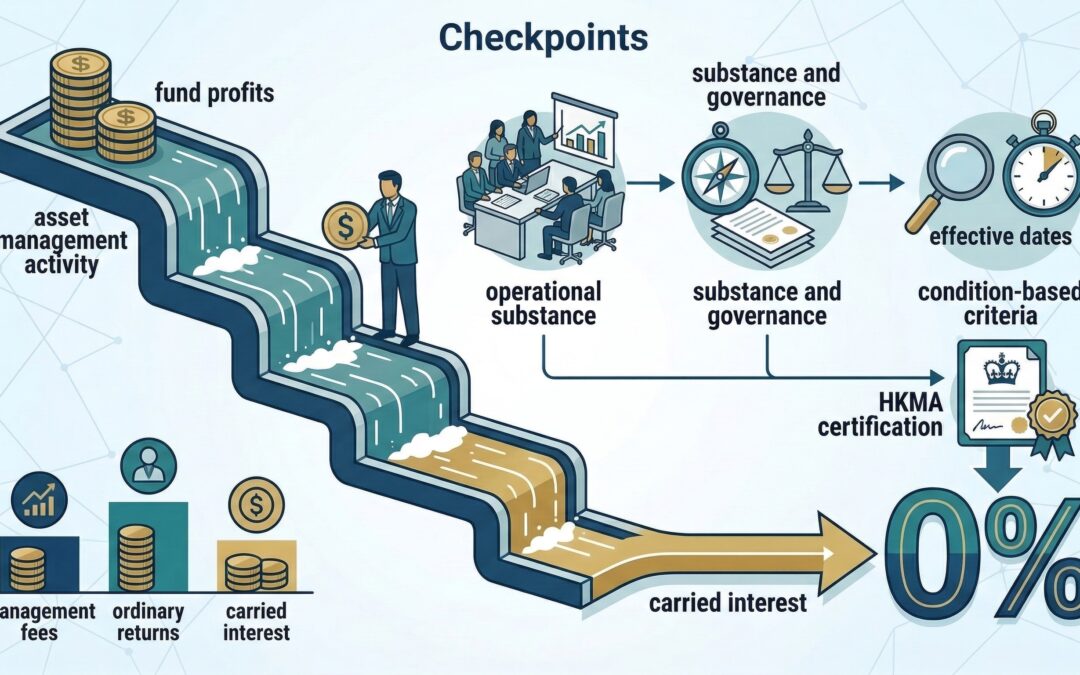

What is “carried interest” (plain English)?

In private equity and similar strategies, carried interest is typically the performance-linked share of profits allocated to the manager/sponsor after certain return thresholds.

This is different from:

– management fees (recurring fees for running the strategy), and

– ordinary investment returns (returns to investors).

—

The headline: 0% profits tax (but only if you qualify)

Hong Kong introduced a carried interest concession regime via legislation enacted in 2021, and the HKMA has issued guidelines on certification of funds under the relevant schedule for the carried interest tax concession.

Practical takeaway:

“0%” is not automatic. It is condition-based.

—

Why this matters for structuring

A carried interest regime affects:

– how you draft the fund’s waterfall,

– how you document “qualifying persons” and services,

– whether the operating model and governance actually match the intended regime.

This is where tax, legal documentation and operations must align.

—

Common pitfalls

Pitfall 1: assuming “LPF = 0% carry”

Vehicle choice alone is not the full analysis. The operating and qualifying conditions matter.

Pitfall 2: substance is treated as an afterthought

If you’re building a Hong Kong platform, operational substance and governance hygiene are not optional.

Pitfall 3: documents don’t match reality

If your waterfall, employment arrangements, approvals and reporting don’t align, you create avoidable risk.

This is also why we stress bankable structures and clean controls:

How to build a “bankable” Hong Kong fund (AML, records, controls)

—

How TITUS + IMSG helps clients implement this properly

TITUS supports:

– structuring and documentation (including carry/waterfall mechanics),

– fund formation and operating agreements,

– regulatory mapping where required.

Our sister team – IMSG supports:

– operational setup and maintenance,

– governance cadence,

– accounting/tax coordination and record hygiene.

If you want to explore whether this is relevant to your strategy, start here:

—

Next step: quick call with our Principal

If you want to discuss a client fact pattern or your firm’s recurring needs, we can set up a quick Zoom call with Michael Titus (Principal, TITUS): https://titus.com.hk/our-people/michael-titus/

Send 2–3 time slots to us via:

Email: info@titus.com.hk, or

Whatsapp: +852 9702 3003

—

Disclaimer: This article is for general information only and does not constitute legal advice. Specific advice should be sought for your particular circumstances.

RELATED READING

– Pillar guide: Hong Kong Funds & Private Investment Vehicles guide

– DIPN 61 (plain English): DIPN 61 explained (Unified Fund Exemption)

– LPF guide: LPF (Limited Partnership Fund) guide

– Bankable structures playbook: How to build a “bankable” Hong Kong fund (AML, records, controls)