Last updated: 13 March 2026

If you’re advising a family, founder, or private capital group with Asia exposure, “just set up an entity” is rarely the hard part. The hard part is building a structure that is:

- legally coherent,

- operationally clean, and

- explainable to banks and counterparties.

This guide is a practical overview of the most common Hong Kong options—how to choose between them, and where deals typically go wrong. If you want to speak to our team about a specific fact pattern, start with our Investment Funds practice page here: Investment Funds practice page

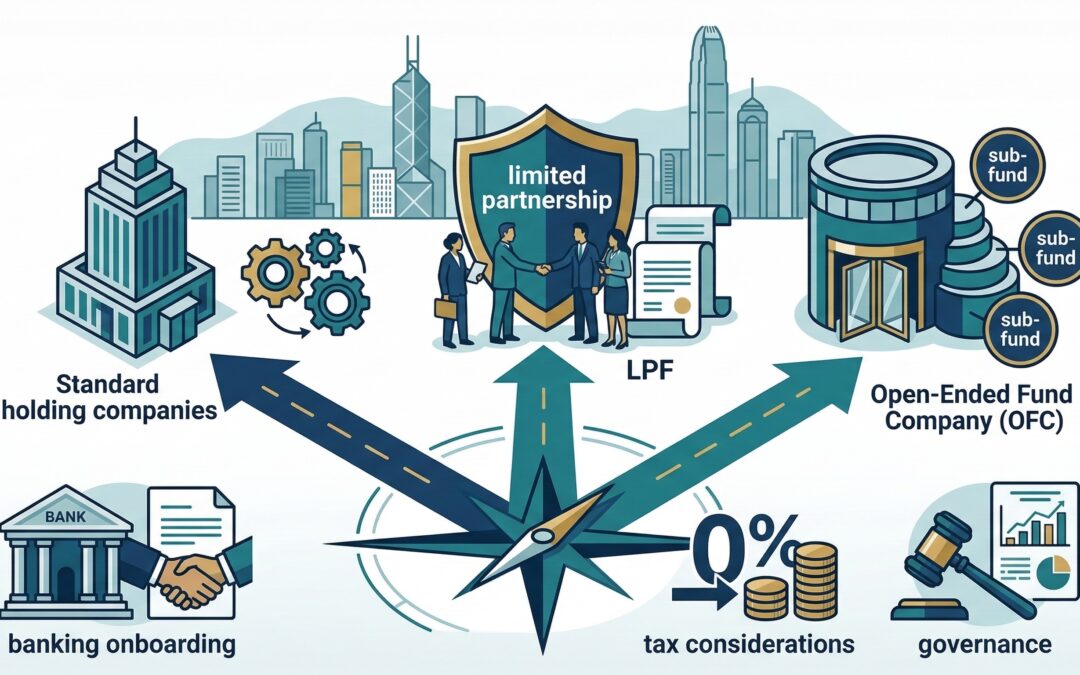

The quick map: LPF vs OFC vs HoldCo + SPVs

Option 1: Holding company + SPVs (the “private investment platform” for most families)

Best when you want a straightforward private investment vehicle to hold assets (portfolio investments, operating companies, property SPVs, co-invest positions) without running a fund-style subscription/redemption model.

Typical characteristics:

– one HK holding company (or a small stack),

– SPVs per asset or strategy,

– governance rules (approvals, signatories, reporting cadence) designed upfront.

Option 2: LPF (Limited Partnership Fund) — private fund-style wrapper

Best when the vehicle behaves like a private fund:

– pooled capital,

– multiple investors (even a small “club”),

– private equity / venture / credit-style economics,

– partnership governance and distribution mechanics.

Read our full LPF guide:

Option 3: OFC (Open-ended Fund Company) — corporate fund wrapper

Best when you want a corporate form fund structure, often with:

– share issuance/redemption mechanics,

– umbrella/sub-fund thinking,

– a compliance design that is closer to institutional fund governance.

Read our full OFC guide:

—

“Why Hong Kong?” — reasons advisers can use without sounding like a brochure

Hong Kong remains a practical Asia hub for private capital structures because it combines:

– a mature legal and professional ecosystem,

– common-law familiarity (helpful for international advisers),

– proximity to Asia capital and banking infrastructure, and

– a growing set of fund-related regimes and guidance.

From a legal-services perspective, the biggest “why” is still execution: if the structure needs to operate with Asia banking, Asia counterparties, and multi-jurisdictional family governance, Hong Kong is often a workable centre of gravity.

(If you’re comparing Hong Kong structures or you’re setting up a fund platform, our team can help you scope the right path here: https://titus.com.hk/investment-funds/)

—

The five questions that decide the structure (90% of the time)

1) Is it really a “fund” — or just a private holding platform?

If investors pool money and a manager runs the strategy, you’re in fund logic. If it’s a family/founder investment platform, a HoldCo/SPV stack may be cleaner.

2) Do you need subscriptions/redemptions (open-ended behaviour)?

If yes, OFC becomes more relevant. If no (closed-end), LPF or HoldCo/SPVs are often more natural.

3) How many investors are there (and how sophisticated)?

A family-only vehicle often prioritises operational simplicity. A club/co-invest vehicle often benefits from LPF mechanics and clearer partner rights.

4) What does the bank need to see?

If your structure can’t be explained and evidenced, onboarding stalls. That’s why “bankability” is not a footnote.

(We cover this in detail here: /bankable-hong-kong-fund-structures-aml-controls/)

5) Are you aiming for any Hong Kong fund tax regimes?

If your vehicle is truly operating as a “fund” and meets the relevant conditions, Hong Kong’s profits tax exemption guidance becomes relevant. Start with our plain-English note:

/dipn-61-hong-kong-profits-tax-exemption-for-funds/

—

Typical timelines (realistic planning)

Every case differs, but these are the planning ranges we see most often:

– HoldCo + SPVs: usually fastest legally; banking and operational setup often drives the real timeline.

– LPF: manageable once key roles are lined up and the LPA terms are clear.

– OFC: more sequencing-heavy; custodian and investment manager decisions should be made early.

—

Common pitfalls (and how to avoid them)

Pitfall 1: building a “paper structure” that doesn’t match real life

If actual control is different from what documents say, problems appear in banking, audits, disputes, and exits.

Pitfall 2: choosing the vehicle before defining governance

The structure should follow the governance plan (who approves what, who can sign, what reporting is required).

Pitfall 3: ignoring the operational layer

Entity maintenance, accounting/tax coordination, record-keeping, and approval logs are what keep the structure alive.

Our Corporate & Commercial practice often supports the “holding and governance” side of these projects:

Our Regulatory practice supports compliance and risk mapping when the facts require it:

—

How TITUS typically supports these structures (the “HK desk” model)

TITUS supports legal design and implementation:

– vehicle selection (LPF vs OFC vs SPVs),

– formation documentation and agreements,

– fund formation and operating documentation,

– regulatory mapping where needed,

– transactions, restructurings, and dispute planning.

Our sister company – IMSG supports the running of the structure:

– company secretarial and filings,

– accounting/tax coordination,

– ongoing operational cadence (records, approvals, reporting),

– practical “bankability” support.

If you’re exploring Hong Kong for a client, start here:

—

Next step: quick call with our Principal

If you want to discuss a client fact pattern or your firm’s recurring needs, we can set up a quick Zoom call with Michael Titus (Principal, TITUS):

Send 2–3 time slots to us via:

Email: info@titus.com.hk, or

Whatsapp: +852 9702 3003

—

Disclaimer: This article is for general information only and does not constitute legal advice. Specific advice should be sought for your particular circumstances.

RELATED READING

– LPF guide: https://titus.com.hk/the-limited-partnership-fund-lpf-in-hong-kong-a-complete-guide/

– OFC guide: https://titus.com.hk/the-open-ended-fund-company-ofc-in-hong-kong-what-you-need-to-know/

– DIPN 61 (plain English): https://titus.com.hk/dipn-61-hong-kong-profits-tax-exemption-for-funds/

– Carried interest (0% profits tax): https://titus.com.hk/hong-kong-carried-interest-tax-concession-0-profits-tax/

– Bankable structures playbook: https://titus.com.hk/bankable-hong-kong-fund-structures-aml-controls/