Last updated: 13 March 2026

Hong Kong’s LPF regime is designed to enable private funds to be registered as limited partnerships in Hong Kong, and it commenced operation on 31 August 2020. (Official overview: https://www.cr.gov.hk/en/legislation/lpf.htm)

This guide focuses on what clients and advisers actually need: the roles you must appoint, the filing workflow, realistic timelines, and what to maintain after launch.

If you want to discuss a specific structure, start here:

—

What is an LPF (and who it’s for)?

An LPF is typically used for private fund-style structures—private equity, venture, credit, real assets, or a “club deal” investment vehicle—where partnership economics (capital commitments, distributions, waterfall/carry) are useful.

If you’re still deciding LPF vs OFC vs a holding/SPV stack, read:

Hong Kong Funds & Private Investment Vehicles guide

—

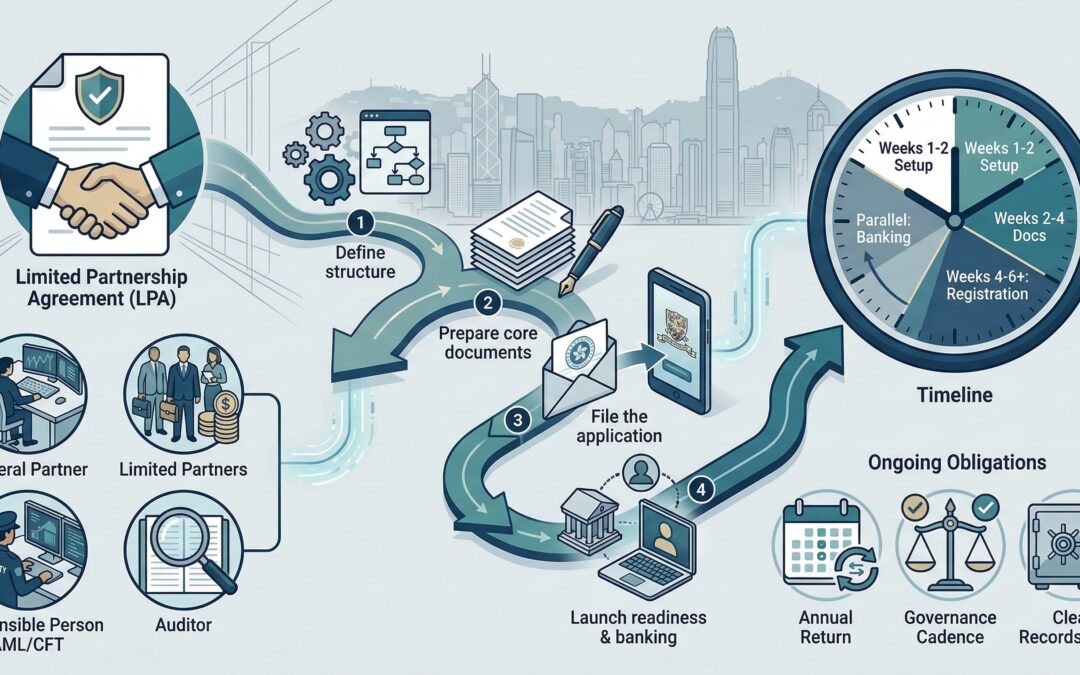

The key roles you need (don’t draft the LPA until these are clear)

1) General Partner (GP) and the Investment Manager

The GP runs the fund and is central to how authority and liability are allocated. Many groups use a corporate GP. Under most scenarios, the GP will delegate the investment management function to a licensed investment manager.

2) Limited Partners (LPs)

LPs contribute capital and receive limited liability treatment, but they should not run the day-to-day management (your governance plan matters here).

3) Responsible Person (AML/CFT)

LPFs require a local AML/CFT compliance arrangement via a “responsible person”. This is one of the first things that banks and counterparties will ask about.

4) Auditor

Annual audited financial statements are a common operational expectation for credible funds, and LPF structures typically plan for audit from day one.

5) Hong Kong solicitor / law firm (for filing)

The Companies Registry’s LPF FAQ states the application must be submitted by a Hong Kong law firm or solicitor on behalf of the proposed GP. (Official FAQ: https://www.cr.gov.hk/en/legislation/lpf/faq_new.htm)

—

Registration steps (practical workflow)

Step 1: Define structure + governance

Before paperwork, lock down:

– who signs bank instructions,

– approval thresholds (investments, borrowings, disposals),

– conflicts policy,

– reporting cadence.

If “bankability” is important (it usually is), read:

How to build a “bankable” Hong Kong fund (AML, records, controls)

Step 2: Prepare core documents

Typical documents include:

– Limited Partnership Agreement (LPA)

– subscription / commitment documents

– service provider agreements (admin, audit, custody if relevant)

– internal governance pack (signatory matrix, approvals log template)

Step 3: File the application

Per the Companies Registry FAQ, an application involves Form LPF1 and specified fees. The FAQ lists:

– registration fee: HK$2,555

– lodgement fee: HK$479 (non-refundable)

– IRBR4 notice to Business Registration Office

– prescribed business registration fee/levy (see IRD table)

(See official FAQ for details: https://www.cr.gov.hk/en/legislation/lpf/faq_new.htm)

Note: The FAQ also notes that items relating to simultaneous business registration applications started from 27 December 2023 in certain cases. (Same official FAQ page above.)

Step 4: Launch readiness (parallel work)

You can usually run in parallel:

– banking onboarding,

– investor onboarding pack,

– operational record-keeping setup.

—

Realistic timeline (what drives it)

Instead of promising “7 days”, we plan around the real friction points:

– Week 1–2: structure, roles, term sheet for LPA, service providers lined up

– Week 2–4: drafting + negotiations + onboarding pack

– Week 4–6: filing + launch readiness

– Banking: may extend timelines depending on complexity, geography, and source-of-wealth documentation

—

Ongoing obligations (what weak LPFs fail on)

The Companies Registry FAQ confirms LPFs have filing and record-keeping requirements, including an annual return (filed by the GP within a specified timeframe). (Official FAQ: https://www.cr.gov.hk/en/legislation/lpf/faq_new.htm)

In practice, what keeps things healthy is:

– a governance cadence (quarterly review, approvals log),

– clean books and audit readiness,

– AML/records hygiene.

This overlaps heavily with regulatory risk management. If your structure has regulated activity concerns or cross-border marketing questions, our Regulatory practice can help:

—

LPF vs OFC (one-minute comparison)

LPF is usually the clean choice when:

– the fund is closed-end / commitment-based,

– you want partnership economics and a private fund wrapper.

If you need a corporate fund structure and are prepared for custodian + investment manager sequencing, look at OFC:

—

Next step: quick call with our Principal

If you want to discuss a client fact pattern or your firm’s recurring needs, we can set up a quick Zoom call with Michael Titus (Principal, TITUS): https://titus.com.hk/our-people/michael-titus/

Send 2–3 time slots to us via:

Email: info@titus.com.hk, or

Whatsapp: +852 9702 3003

—

Disclaimer: This article is for general information only and does not constitute legal advice. Specific advice should be sought for your particular circumstances.

RELATED READING

– Pillar guide: Hong Kong Funds & Private Investment Vehicles guide

– OFC guide: OFC (Open-Ended Fund Company) guide

– DIPN 61 (plain English): DIPN 61 explained (Unified Fund Exemption)

– Carried interest (0% profits tax): Hong Kong carried interest tax concession (0% profits tax)

– Bankable structures playbook: How to build a “bankable” Hong Kong fund (AML, records, controls)